The FSM Social Security Administration wishes to invite all interested FSM citizens working abroad to participate in the program. Public Law 14-86, which was passed on October 23, 2006, created a new provision within the social security law that would allow a citizen of the FSM working abroad to voluntarily contribute into the system to earn the right to benefits. FSM citizens who are actually working outside of the FSM, Palau or Marshalls can make voluntary contributions. In order for an abroad citizen to apply for Voluntary Contribution through the ACH, our official website – www.fsmssa.fm has prepared printable forms to (1) enroll in the program, (2) authorize the transactions, and (3) to authorize retroactive payments. Once these forms are filled and sent to the main office for processing, FSMSSA will collect their quarterly taxes from their account through online ACH. After every transaction, a receipt will be sent to the contributor while the bank documents the transfer in the contributor’s passbook.

For persons who are self-employed or regular employees outside of the FSM, Republic of Palau and Republic of the Marshall Islands, they may make voluntary contributions to receive quarters of coverage and to accumulate payments to their minimum contribution requirements, even if they are contributing to another Social Security system. The person must make payments to FSM SSA in the FSM, and file a quarterly return. Any person making these voluntary contributions is subject to the same deadlines as any other taxpayer. The person must also pay both the employee and employer’s share of the social security tax. The quarterly earnings are fixed at $1,250.00

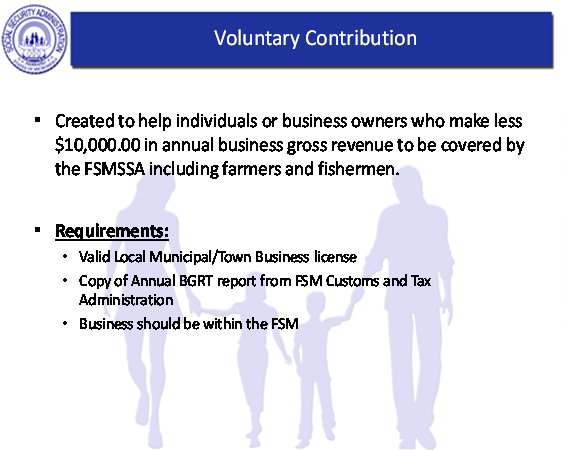

It applies also to FSM citizens now.

For persons who are self-employed sole proprietors with no employees in the FSM, which can include farmers and fishermen, and who make less than $10,000.00 per year, may make contributions to the Social Security System. The person will be deemed to make $1,250.00 per quarter, and they must pay the employee and the employer’s share. After January 1, 2013, the payment is $93.75 for the employee’s share and $93.75 for the employer’s share, totaling $187.50 per quarter. Any self-employed person electing to make such voluntary contributions must file quarterly returns and is subject to the same deadlines as any other taxpayer. If revenue received by a self-employed person is $10,000.00 or more, they are subject to the regular mandatory contribution provisions.